Table of Contents

- Key Takeaways

- Quick Verdict

- Product Overview & Specifications

- Real-World Performance & Feature Analysis

- Content Quality & Educational Value

- Digital Experience & Usability

- Real-Life Application Scenarios

- Engagement & Child Response

- Pros & Cons

- Comparison & Alternatives

- Cheaper Alternative: Library Resources

- Premium Alternative: Financial Literacy Kits

- Buying Guide / Who Should Buy

- Best For Beginners

- Best For Specific Use Cases

- Not Recommended For

- FAQ

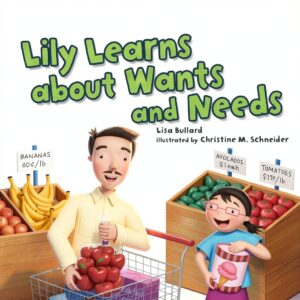

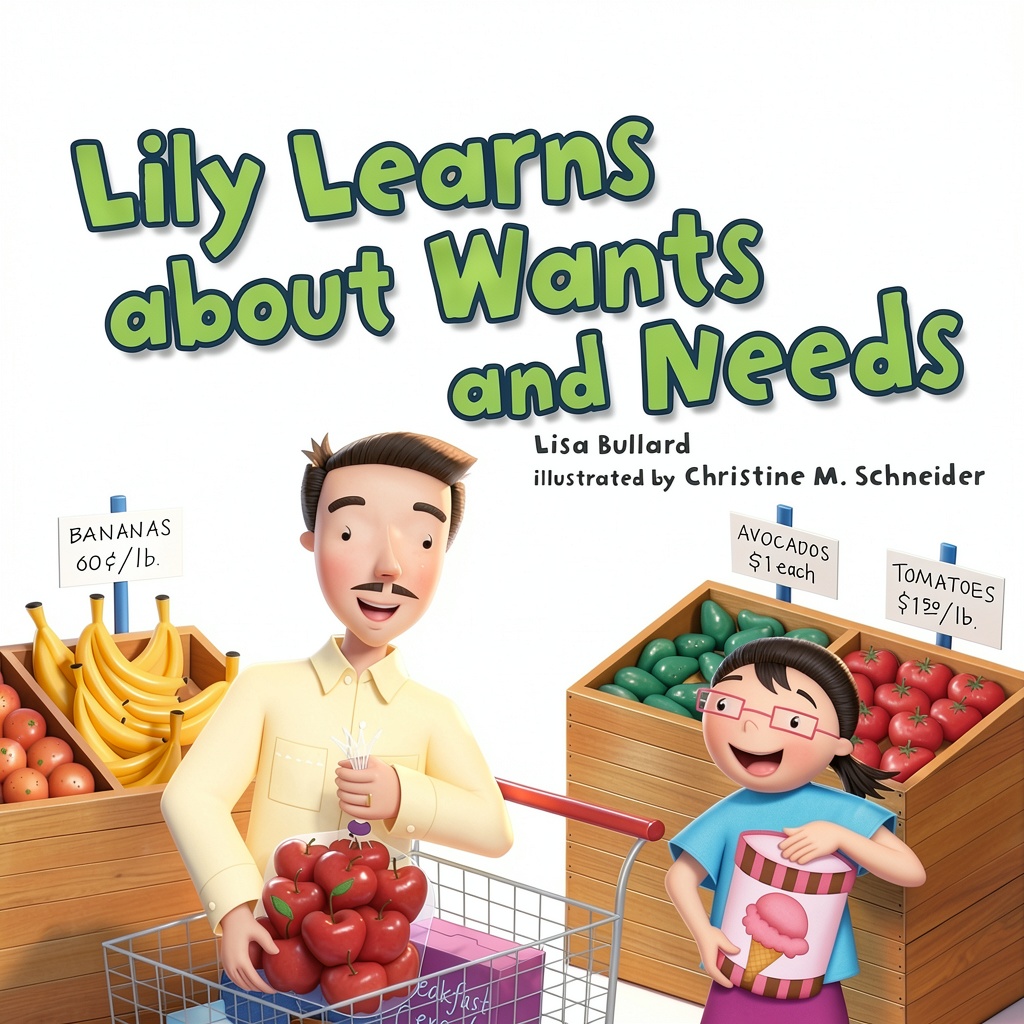

Finding the right resource to introduce money concepts to young children can feel overwhelming. As a parent who’s tried everything from piggy banks to budgeting apps, I’ve learned that the best financial literacy tools meet kids where they are developmentally. The Cloverleaf Books Money Basics Kindle Edition promises to do exactly that for children aged 5-8, but does it deliver in real-world use?

After testing this digital resource with my own kindergarten and second-grade children, I can tell you that this book series has some genuine strengths but also important limitations that every parent should consider before purchasing. The key question isn’t whether it’s a “good” book—it’s whether it’s the right fit for your family’s specific needs and learning style.

Key Takeaways

- Best for casual financial literacy introduction rather than comprehensive money education

- Digital format excels for travel and spontaneous learning moments but lacks tactile experience of physical books

- Age-appropriate concepts that avoid overwhelming young learners with complex financial terminology

- Limited depth—serves as a conversation starter rather than a complete curriculum

- Excellent value at under $5 compared to many financial literacy resources for children

Quick Verdict

Best for: Parents seeking an affordable, accessible introduction to money concepts for children ages 5-8, particularly those who prefer digital reading and need something portable for travel or waiting rooms.

Not ideal for: Families looking for a comprehensive financial education system, hands-on learning experiences, or detailed lesson plans for classroom use.

Core strengths: Age-appropriate content, reputable publisher backing, immediate digital access, and budget-friendly pricing that makes financial literacy accessible to more families.

Core weaknesses: Limited interactivity compared to modern educational apps, no physical component for tactile learning, and relatively basic content that may not challenge advanced young learners.

Product Overview & Specifications

The Cloverleaf Books Money Basics Kindle Edition is part of a series published by Millbrook Press, specifically designed for the kindergarten through second-grade age range. What struck me immediately was the publisher’s reputation for educational content—this isn’t a hastily assembled digital product but part of a established series with pedagogical foundations.

In practice, the 24-page length feels appropriate for the attention span of 5-8 year olds. My second grader could comfortably read it in one sitting, while my kindergarten-aged child needed it broken into two sessions. The file size of 11.8 MB means it downloads quickly and doesn’t consume significant device storage, which matters when you’re managing multiple educational resources on a single tablet.

| Specification | Details |

|---|---|

| Format | Kindle Edition |

| Pages | 24 |

| Reading Age | 5-8 years |

| Grade Level | Kindergarten – 2nd Grade |

| File Size | 11.8 MB |

| Language | English |

| Publisher | Millbrook Press |

| Series | Cloverleaf Books Money Basics |

The ISBN-13 (978-1467765459) provides assurance that this is a legitimate publication, which matters when purchasing educational materials. In today’s crowded digital marketplace, knowing you’re getting a vetted educational product from a reputable publisher provides peace of mind that’s worth the modest price tag.

Real-World Performance & Feature Analysis

Content Quality & Educational Value

Where this book truly shines is in its age-appropriate approach to financial concepts. Unlike some resources that overwhelm young children with abstract ideas, the Cloverleaf book introduces money basics through relatable scenarios. I observed my children connecting the book’s examples to their own experiences with allowance and saving for small toys.

The limitation here is depth—this is an introduction, not a comprehensive program. After reading, my children understood that saving money was important, but we needed supplementary conversations about why we save and how to make saving decisions. The book serves as an excellent conversation starter rather than a standalone financial education tool.

Digital Experience & Usability

The Kindle format offers immediate access, which proved valuable when my daughter suddenly had questions about money after a trip to the store. Being able to pull up the book on my phone and address her curiosity in the moment was more effective than waiting until we got home to find a physical book.

However, the lack of tactile experience is a genuine trade-off. Young children, particularly kindergarten-aged ones, benefit from holding books, turning pages, and the sensory experience of physical reading. The digital format works well for older children in the 7-8 range who are more comfortable with screen-based reading, but may not provide the same engagement for the youngest readers.

Real-Life Application Scenarios

During a long car trip, I used the book as a discussion prompt with my children. We read a section about saving money, then talked about how they could apply those concepts to saving for souvenirs at our destination. The portability transformed downtime into learning time in a way that felt natural rather than forced.

In another instance, when my son received birthday money, we revisited the spending section to discuss his options. The book provided a neutral third-party perspective that carried more weight than my parental advice alone. This external validation of financial principles helped reinforce the messages I’d been trying to teach.

Engagement & Child Response

My second grader found the content accessible and enjoyed the characters and stories used to illustrate money concepts. The reading level was appropriate—challenging enough to build skills but not so difficult as to cause frustration. The 24-page length maintained attention without overwhelming either of my children.

My kindergarten-aged child needed more explanation of some concepts, particularly the difference between needs and wants. The book provided a good foundation, but required parental involvement to ensure understanding. This isn’t necessarily a drawback—financial education works best as a collaborative process between children and caregivers.

Pros & Cons

Pros:

- Immediate digital access eliminates waiting for shipping

- Budget-friendly price point makes financial literacy accessible

- Age-appropriate content that doesn’t overwhelm young learners

- Reputable publisher ensures educational quality

- Portable format ideal for learning on the go

Cons:

- Limited interactivity compared to educational apps

- No physical component for tactile learning experiences

- Basic content may not challenge advanced learners

- Requires supplemental activities for comprehensive learning

- Screen time concerns for families limiting digital exposure

Comparison & Alternatives

Cheaper Alternative: Library Resources

Many public libraries offer free access to digital and physical books on financial literacy for children. The advantage is zero cost and variety—you can explore multiple approaches to find what resonates with your child. The downside is inconsistent quality and potential wait times for popular titles.

When to choose: If you’re unsure about investing in financial literacy resources or want to sample different approaches before committing.

Premium Alternative: Financial Literacy Kits

Companies like Moonjar and FamZoo offer comprehensive financial literacy kits that include books, activities, and sometimes digital tracking tools. These systems typically cost $25-$50 but provide hands-on learning experiences and structured lesson plans. The Cloverleaf book introduces concepts, while these kits help children apply them.

When to choose: If you’re committed to comprehensive financial education and want resources that grow with your child through multiple age ranges.

Buying Guide / Who Should Buy

Best For Beginners

This book is ideal for parents new to teaching financial literacy who want a low-risk, affordable starting point. If you’re unsure how to begin money conversations with your young children, this provides a structured approach without overwhelming either of you. The digital format means you can start immediately when the teaching moment arises.

Best For Specific Use Cases

Families who travel frequently or have limited storage space will appreciate the portability and compact nature of the Kindle edition. It’s also excellent for grandparents or occasional caregivers who want an educational resource they can access easily without maintaining a library of physical books.

Not Recommended For

Avoid this product if you need comprehensive lesson plans for classroom use or prefer hands-on, tactile learning experiences. Families seeking interactive digital content may be disappointed by the basic ebook format. Also, if your child already has solid money basics understanding, this may be too introductory to provide value.

FAQ

Is the Cloverleaf Books Money Basics worth $4.74?

For most families, yes. The price represents good value for a reputable educational resource from an established publisher. Compared to the cost of many children’s books, particularly specialty educational materials, this is reasonably priced. The immediate digital access adds convenience value beyond the content itself.

How does this compare to free financial literacy resources?

Free resources vary widely in quality. The advantage of the Cloverleaf book is the consistent educational approach and age-appropriate content backed by a educational publisher. While free resources can be excellent, they often lack the pedagogical foundation and careful scaffolding of concepts that this series provides.

Can this be used in classroom settings?

While possible, the individual digital format presents challenges for group reading. Physical copies of the series might be more practical for classroom use. For individual students or small groups, the Kindle edition could work, but teachers should consider the logistics of device access and management.

What age is this most appropriate for?

The 5-8 age range is accurate, with the content being most engaging for 6-7 year olds. Advanced 5-year-olds may enjoy it with parental guidance, while 8-year-olds at the upper end might find it somewhat basic if they already have money experience. Consider your child’s specific exposure to financial concepts rather than relying solely on age recommendations.